|

1

|

- Church and Charity Law Seminar

November 14, 2013

|

|

2

|

- Understanding the Regulator

- Our Approach to Compliance

- Common Compliance Issues

- Steering Clear of Compliance Concerns

|

|

3

|

- Two sources of law:

- Income Tax Act - outlines requirements and obligations of charitable

registration

- Court decisions - determines what purposes and activities are

charitable

- Canada Revenue Agency’s interpretation of the law expressed through

policy guidance

|

|

4

|

- Charitable sector

- Diverse range of entities

- Public

- Donors, taxpayers/Canadians

- Professionals/ Intermediaries

- Lawyers, accountants, fundraisers

|

|

5

|

- Facilitating voluntary compliance

- Education - website, guidance products, webinars

- Client services, including telephone support

- Assisting compliance

- Application review and advice

- Annual information return follow-up

- Enforcing compliance

- Field audits and litigation (outcomes - education letters, compliance

agreements, sanctions, revocation)

|

|

6

|

- Audit Program

- Approximately 1% of charities audited each year

- Types of Audits

- Office Audits - conducted out of

headquarters

- Field Audits - conducted at the charity’s premises

|

|

7

|

- Random audits

- High risk files

- Audit projects to review specific issues or concerns

- Compliance agreement follow-ups

- Exploratory audits

|

|

8

|

|

|

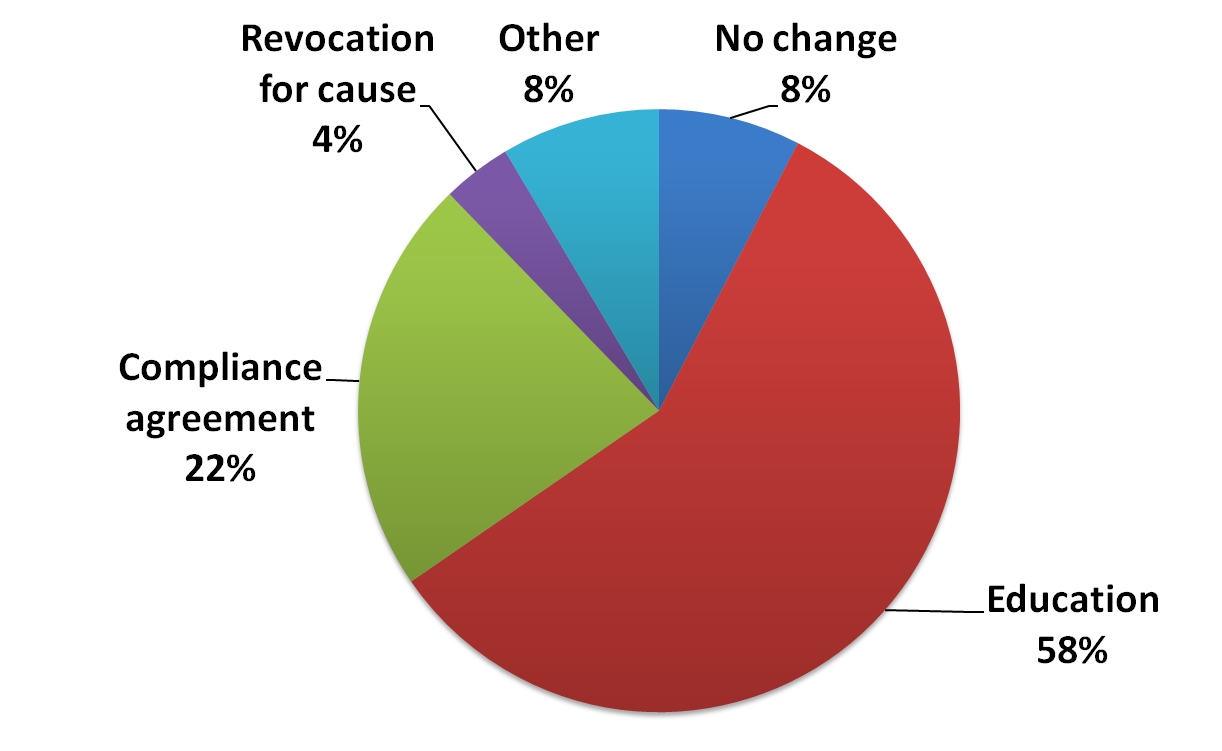

9

|

- Provide opportunity to correct compliance issue

- Consider whether non-compliance is

intentional or unintentional

- Utilize compliance agreements

- Apply sanctions or revocation where warranted

|

|

10

|

|

|

11

|

- Improper receipts - important elements missing;

- Receipting for services - not permitted;

- Not properly establishing fair market value;

- Inadequate books and records to verify receipts, revenue and

expenditures

|

|

12

|

- Schools that are registered charities may issue receipts for religious

tuition fees if they:

- Teach religion exclusively; or

- Operate in a dual secular/religious capacity

- Receipts may be issued for the religious portion of tuition fees

- See IC 75-23 for more information

|

|

13

|

- Registered charities may only use their resources in two ways:

- By carrying on their own charitable programs; or

- By making gifts to qualified donees

- Gifting to non-qualified donees is a serious issue

|

|

14

|

- A charity that operates through an intermediary must maintain direction

and control over its resources

- A properly structured agreement helps demonstrate direction and control

- Even when agreement exists, charities sometimes fail to properly

implement and monitor

|

|

15

|

- Charities cannot have political purposes

- A charity may carry out a limited amount of political activity provided

they are:

- Connected to the charity’s purpose

- Subordinate to the charitable purpose

- Non-partisan in nature

|

|

16

|

- Establish internal controls and policies for receipting and expenditures

- Ensure direction and control by:

- Written agreements

- Monitoring and supervising

- Clear and complete instructions

- Separation of funds

|

|

17

|

- Client service

- Call centre, written enquiries

- Website

- Guidance products, information on operating a registered charity

- Sector outreach

- Information sessions, webinars, electronic updates and newsletters

|

|

18

|

- Client Services - General Inquiries

- 1-800-267-2384

- Charities Information on the Web:

- www.cra.gc.ca/charities

- Charities Electronic Mailing List:

- To connect, go to our Website main page, bottom right, and click on

“Email list sign-up”

|

Notes

Notes{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}